Restricted Stock Units: Life Cycle

The following hypothetical example outlines the entire life cycle of an RSU grant.

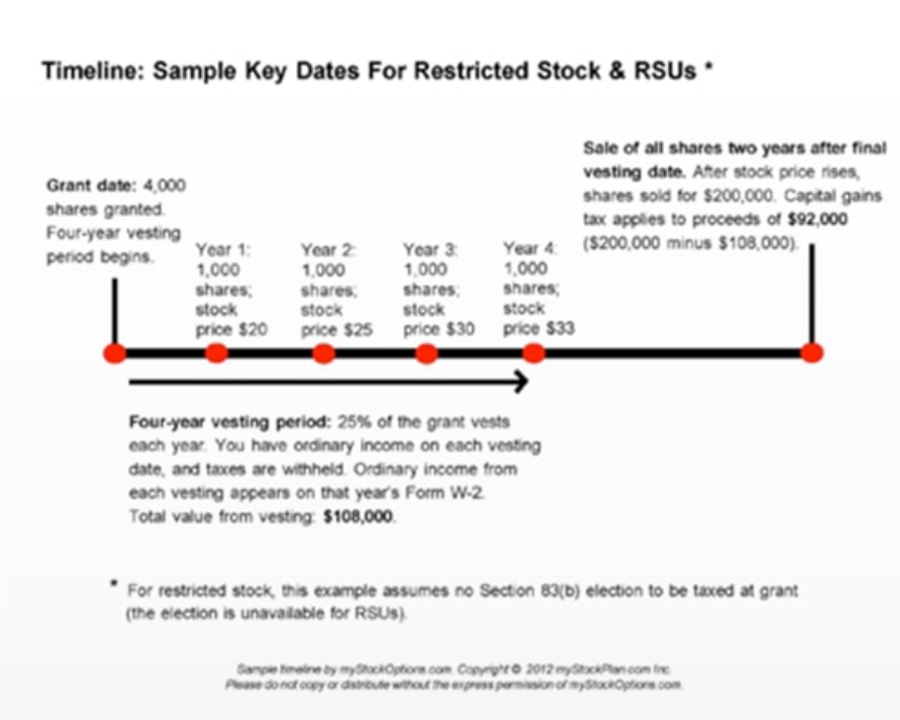

Your company grants you 20,000 RSUs that vest at a rate of 25% a year. The market price at grant is $18.

One year after the grant, 25% of the shares vest and the stock price is $20 (5,000 x $20 = $100,000 of ordinary income). The following year another 25% of your share’s vest when the stock price is $25 (5,000 x $25 = $125,000). Three years after the initial grant another 25% vest when the stock price is at $30 (5,000 x $30 = $150,000 of ordinary income). Year four your final 25% of shares vest at a stock price of $35 (5,000 x $35 = $175,000 of ordinary income). The total value of all your RSU after vesting is $550,000, and each increment is taxable on its vesting date as compensation income when the shares are delivered.

Let’s assume you pay the tax due each year out of pocket and don’t surrender shares back to the company to pay taxes. At a later date you sell the stock when the price is at $40 ($800,000 for the 20,000 shares). Your capital gain is $250,000 ($800,000 minus $550,000), which is reported on your tax return on Form 8949 and Schedule D. If you hold the shares for more than one year after share delivery, the sales proceeds will be taxed at the long-term capital gains rate, which is a considerable lower rate than short term capital gains.

Although RSU’s are more complex then salary compensation, they can be a great way to participate in the growth and success of the company. When making decisions around your RSU’s, it is important to consult with your tax professional.

;)